In 2026, personal loans in the USA remain a top-searched financial product for millions of Americans facing rising living costs, credit card debt, emergencies, medical bills, home improvements, or big purchases like engagement rings or travel. These flexible, unsecured loans provide quick funding without collateral, making them ideal for debt consolidation or major expenses. However, many borrowers overpay due to misunderstandings about APR (Annual Percentage Rate), hidden fees, and lender strategies.

If you’re navigating the “new normal” of elevated but stable interest rates after the Federal Reserve’s 2025 cuts (holding steady at 3.50–3.75%), this complete guide explains personal loan interest rates in the USA 2026, factors affecting them, common fees, top lenders, economic forecasts, and expert tips to secure the lowest APR personal loans. We’ll also cover trends like AI-based approvals and how to avoid scams. (Note: Rates as of early February 2026; verify with lenders for personalized offers.)

Whether you’re a first-time borrower or looking to refinance, smart planning can save thousands in interest. Let’s break it down.

Current Personal Loan Interest Rates in the USA (February 2026)

Personal loan rates in the USA are shown as APR, which includes interest + fees for a true cost picture. As of early 2026, averages have dipped slightly from late 2025 due to Fed stability, but vary widely by credit score, loan term, amount, and lender type.

- Overall Average APR: Around 12.26% for a typical $5,000, 3-year loan with a 700 FICO score (Bankrate data as of Jan. 28, 2026).

- By Term (Credible marketplace data, week ending Jan. 25, 2026):

- 3-year loans: 13.06% average.

- 5-year loans: 18.46% average.

- Short-Term Rates: ~11.65% for 24-month loans at commercial banks (Federal Reserve trends stable into 2026).

- Full Range: Lowest APR as low as 6.49% (with autopay and excellent credit) to highs of 35.99%+ for high-risk borrowers.

Shorter terms (2–3 years) generally offer lower APRs than longer ones (5+ years) due to reduced lender risk. Personal loans beat credit cards (average ~20%+ APR), especially for consolidation.

Average APR by Credit Score (2026 Data)

Your credit score is the biggest factor in personal loan interest rates USA 2026—lenders use risk-based pricing, so even small improvements can drop your APR significantly.

| Credit Score Range (FICO) | Rating | Average APR (3-Year Term) | Average APR (5-Year Term) | Notes |

|---|---|---|---|---|

| 800+ | Excellent | 10.87%–11.77% | 15.75% | Best rates; often single-digit with discounts. “Unicorn” rates around 8-9% for premium borrowers. |

| 740–799 | Very Good | 13.73%–14.74% | 18.69% | Competitive; lower than good credit. |

| 670–739 | Good | 20.21%–22.72% | 23.72% | Higher than excellent; still viable for many. |

| 580–669 | Fair | 29.13%–30.17% | 30.98% | Elevated rates; consider alternatives. |

| Below 580 | Poor | 25.0%–36.0%+ | N/A | High rates or limited approval; focus on credit repair. |

These are averages from sources like Credible, LendingTree, and NerdWallet. Excellent credit (720+) unlocks the lowest APR personal loans, while fair/poor scores face 20%+ premiums.

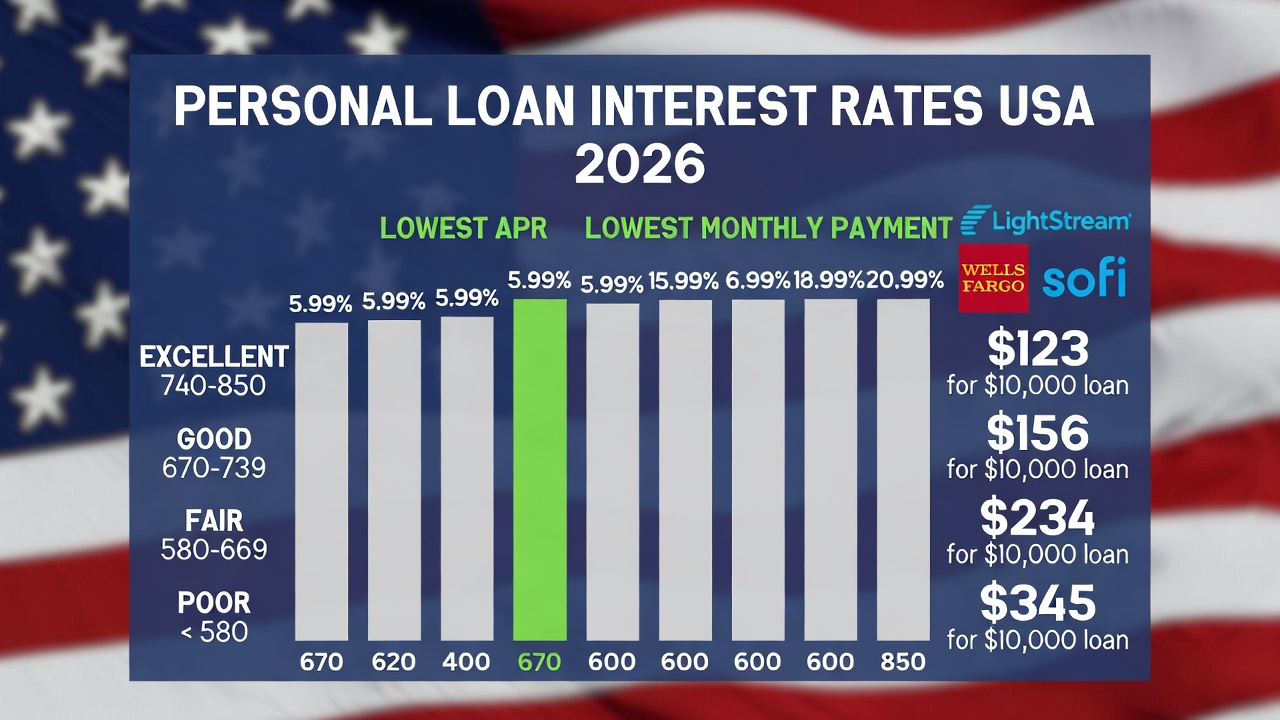

Top Lenders for Lowest APR Personal Loans in 2026

Different lenders cater to various borrower profiles. Online fintech lenders compete aggressively with low fees, while banks and credit unions offer perks for members.

- LightStream: Starting at 6.49% APR (with autopay; no fees; best for excellent credit and home improvements).

- Wells Fargo: As low as 6.74% (relationship discounts; strong for existing customers).

- SoFi: From 8.74%–35.49% (autopay discounts; ideal for good credit and debt consolidation).

- Discover: 7.99%–24.99% (no origination fees; flexible terms).

- PenFed (Credit Union): Competitive under 18% by law; great for members with fair credit.

- Others: Upstart (AI-based for fair credit), Upgrade, Marcus by Goldman Sachs.

For excellent credit (740+): SoFi or LightStream. For fair credit (600–670): Upstart or credit unions like Navy Federal.

2026 Economic Forecast: Will Rates Drop?

The verdict: Likely stabilization, not dramatic drops. The Fed expects modest cuts in Q3/Q4 2026, but lenders have priced this in. Waiting for a 0.5% drop isn’t wise if you have high-interest debt (e.g., 22%+ credit cards)—consolidate now for immediate savings.

Lender tightening means qualifying for advertised lows is harder. Focus on your profile over timing.

Key Factors Affecting Personal Loan APR in the USA

Rates depend on economy and policies controlled by the Federal Reserve, but your profile dominates:

- Credit Score (Most Important Factor): FICO score plays the biggest role—750+ gets lowest APR; below 650 risks high rates or rejection.

- Debt-to-Income (DTI) Ratio: Shows how much income goes to EMIs. Below 36% best; above 43% means higher APR.

- Income & Employment Stability: Stable, high income = low risk = better rates.

- Loan Amount & Term: Shorter tenure (e.g., 24 months) = lower APR but higher EMI; longer = lower EMI but higher total cost.

- Lender Type: Fintech (SoFi, LightStream) for competitive APR; credit unions for capped rates.

Fixed vs. Variable APR: Fixed is safest for beginners (EMI stays same); variable risks changes but may start lower.

Common Fees to Watch in Personal Loans (2026)

Don’t just chase low interest—APR includes fees for total cost. Hidden fees can make a “cheap” loan expensive.

- Origination Fees: 1%–8% (deducted upfront; common with fintech like Upgrade/Upstart). Example: $10,000 loan with 5% fee = $9,500 received, but interest on full amount.

- Late Payment Penalties: $15–$40 or 5% of payment.

- Prepayment Penalties: Rare (avoid lenders like this; most like LightStream/SoFi allow early payoff free).

- Other: Returned payment charges; no application fees usually.

Tip: Use lender calculators for total cost. IRS rules: Personal loan interest generally isn’t tax-deductible (exceptions per Internal Revenue Service).

How to Get the Lowest APR Personal Loan in the USA (5 Tips to Hack Your Rate)

In a high-rate environment, be proactive to force competition. Here’s a 5-step strategy:

- Check & Improve Credit Score: Aim for 720+. Review free reports at AnnualCreditReport.com, pay on time, keep utilization <30%, avoid hard inquiries. (Hindi: Credit card balance 30% se kam rakho; on-time payments history banao.)

- Lower DTI Cleanup: Pay down revolving debt (credit cards) before applying to boost score and approval odds.

- Prequalify & Compare Multiple Lenders: Use soft-pull tools on Bankrate, NerdWallet, Credible, or LendingTree for 4–6 quotes (no score damage). Online comparison gives lower APR, flexible terms, fast approval. (Hindi: Pre-qualification me soft credit check hota hai—score damage nahi hota.)

- Choose Shorter Term & Right Purpose: 24–36 months cuts APR 2–4% vs. 60 months if affordable. Debt consolidation loans often have lower APR than general ones.

- Grab Discounts & Alternatives: Autopay (0.25–0.50% off), direct deposit perks. Add co-signer (with 760+ score) to drop from 22% to 12%. For fair credit: Secured loans (collateral like savings) slash 5–8%; no-cosigner options via AI.

Shop strategically: Apply in 14–45 days for bundled inquiries. Avoid scams—stick to reputable lenders; no “guaranteed” approvals without checks. (Hindi: Scam loan websites se bachna zaroori hai.)

2026 USA Personal Loan Trends

- AI-based credit approval and personalized APR based on spending.

- Instant/same-day funding and fully digital onboarding.

- No-cosigner loans growing.

- Fintech trend: Quick approval, no branch visits.

Final Thoughts for 2026 Borrowers

The “free money” era is over, but smart borrowers can still find competitive lowest APR personal loans in USA 2026. With averages at 12–13% and lows under 7% for excellent profiles, success comes from comparison shopping—the difference can save $2,000+ on a $20,000 loan.

Personal loans are a powerful tool if used wisely for debt consolidation or needs. (Hindi: Right planning = low interest + stress-free repayment.) Before applying: Compare APR, understand fees, improve credit, check EMI affordability.

Ready to find your lowest APR? Prequalify today—no commitment, no credit hit. Verify details with lenders as offers change.